On the day that the FTSE Index goes testicles first down a slope to hell, here is my good news.

The whole idea behind me creating the MoneyTrainers platform is to educate you in the areas of money, making it – hanging on to it – importantly making it work for you.

In order to do this, you will need to think and act differently to everyone around you – and be more like the people who have found wealth or true financial independence. Making your money work hard for you instead of working hard for everyone else is something you will need to do.

With that in mind here are a couple of things you should do.

Two things when considering investments. The first is always to make sure that any investment provides you with a potential return in two ways.

These are income and the potential for capital growth.

The second is to invest when you are ready and not when others tell you should or on the date, the direct debit is taken (what the industry calls pound cost averaging).

With that in mind, the investment markets have been a little bit mad of late (that means they are probably going down). Uncertainty on the planet means that fear creeps in, Brexit, Trump, Russia and now Coronavirus.

The markets, of course, get all ‘doom and gloom’ and the sell-off starts.

If you are fully invested, then that means your net worth is falling as we speak. One of the things you will learn working with me is that you should never be fully invested and certainly not in one place.

Quite simply because being fully invested means you can’t take advantage of the opportunity presented when the world and his dog are shitting themselves due to x or y. All things eventually pass, wars end, pandemics end up with a cure. Elections are held. The shit flow slows.

Problem is we just don’t know when, but we know they will. Eventually, markets bounce back, return to normality (whatever that is).

With this in mind, here is the graph from one of my fav funds. It’s an ETF – more on that elsewhere (like a share but it’s made up of shares in many other companies) it produces income – currently, around 5% (probably 6% with the current dip in the price) has stupidly low investments costs and is managed by a computer not a person. Nowt wrong with people but not a good fit for this.

Let’s have a look at how you could make this work for you.

I make the assumption that you have the cash to invest – you should never ever, be fully invested.

Income EFT – Black Rock.

At the moment 28/2/2020 this investment is down in value quite substantially. But the income yield has remained pretty consistent of course it would – there are different fundamentals in place.

The lower the price is, the more shares you can buy for your given investment amount and the better your income. By investing you effectively transfer pounds for shares, income is paid per share, the more shares you own the more income you’ll get. The lower the price you pay, the more shares and the more income.

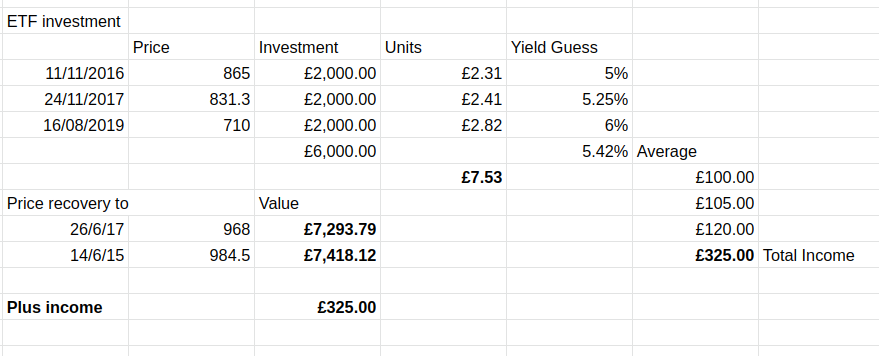

We also know that investment markets will continue to go up and down and we have no control of that as investors. But we can control how much we pay in charges, how much we invest and when. With that in mind, please see the screenshot below where you can see for yourself the impact of buying at the right time.

Assumptions made, you Invested 2016/2017/2019 on the lower valuations. Remember you don’t need to invest when the markets are at the highest price so buying when low makes sense.

The markets always fall and bounce back – we don’t know when or how – but they always do. Sure, I get that you may think this is just hope. Hope that the markets go back up, there is evidence that they will, but sure I understand why you would think like, but…

The income is still being paid from this investment which is guaranteed to make up for some of the losses, you will never be fully invested based on my rule. So if the markets don’t bounce back today it’s not a train smash income is still being paid and you can still buy at a lower price.

And when they do recover back to historic prices and beyond the returns are fantastic.

In this case, a return to 2017 levels means a return of £1,293 plus £325 income making a total return of £1618 on a £6k investment. Of course, there is a charge on this investment of .40% per year which will reduce some of the returns.

I hope this makes sense to you and will get you to take some action on this. Get in touch, ask your boss if we can arrange a workshop (a modest charge) for groups of up to 20.

Contact me here

This money stuff is far simpler than think. You just need to understand it a little more.

Really.

Get in touch as soon as possible, get your own workshop booked.