Inflation Shock.

Bank of England Increases Interest Rates.

Book Recommendation.

Pension Scheme Liabilities Government Nightmare.

Mortgages and deposit rates.

I was going to talk about #lockdownfiles ‘#rishitaxreturns #budget2023 most of which has been discussed everywhere else so nothing from me on any of that.

There was no news in the Budget 2023 that made any sense. Fiddling whilst Rome burns springs to mind. The need for wholesale reform is greater now than ever but I don’t think we’ll see any change.

We have record tax receipts and record levels of taxation. A client this week was explaining to me that she was really worried about a Labour Government coming in. Why? I asked.

She explained that they would increase taxes substantially. Not sure how much higher they can go I explained. They are squeezing until people think they are better off not working. I can’t see how any Government could be any worse.

This quote from Reagan makes more sense now.

“Government is like a baby. An alimentary canal with a big appetite at one end and no sense of responsibility at the other.” – Ronald Reagan.

As I have said before. The Conservative plan is to leave the incoming Government a poison chalice of mess – the new Government won’t be able to sort out the mess in a five-year term – and they hope we’ll have forgotten about Boris, record taxation… By the time the next election comes around.

Inflation Shock. No one expected that.

February 2023 – inflation is 10.4% year-on-year. Well, when I say no one I mean those who are supposed to expect it. Treasury, Bank of England or highly qualified economists.

The rest of us, those doing our own shopping. We see it every day.

We are told UK inflation has gone up mainly due to the following reasons:

- The rise in the cost of energy. The price of gas and electricity has increased significantly in recent months, which has pushed up the cost of living.

- The rise in the cost of food. The price of food has also increased in recent months, due to a number of factors including the war in Ukraine, which has disrupted global supply chains.

- The rise in the cost of services. The cost of services such as transportation, healthcare, and education has also increased in recent months.

The solution, UK government has taken a number of steps to try to reduce inflation, including:

- Raising taxes. The government has raised taxes on income and businesses, which is expected to reduce consumer spending and help to bring down inflation.

- Reducing spending. The government has also reduced spending on public services, which is expected to reduce demand and help to bring down inflation.

- Increasing interest rates. The Bank of England has raised interest rates, which is expected to make it more expensive to borrow money and help to reduce consumer spending.

So, given that inflation has been caused by [insert any reason here] how are the proposed solutions going to reduce it?

No I don’t know either.

Back In The Day. Roman Times Repeated.

Diocletian took the throne in AD 284 and soon faced economic problems. The Empire’s armed forces were enlarged to repel barbarian invasions, but this led to a huge building program and raised taxes. The government also employed more officials, which increased the tax burden. Forced labour was also used to complete many of Diocletian’s public works programs.

Diocletian blamed the inflation on merchants and speculators, but some historians believe that his debasement of the currency was a major cause. The denarius, the standard Roman coin, was debased with tin and copper, which reduced its value. This led to Gresham’s Law, where silver and gold coins were hoarded and left circulation.

The value of the denarius fell by 95% between AD 284 and AD 305. This led to a rise in prices, which made it difficult for people to afford basic necessities. The middle class was almost wiped out, and the poor were hit the hardest.

Diocletian tried to address the inflation by issuing an Edict on Prices and Wages. This fixed the maximum prices that could be charged for goods and services. It also set the maximum wages that could be paid. However, this was largely ineffective, as people continued to trade at higher prices.

Diocletian’s reign was a time of economic turmoil for the Roman Empire. His policies were well-intentioned, but they had unintended consequences that made the situation worse.

Sound familiar?

The Bank of England printed £875bn into the economy under its QE programme.

If you had a money machine in your back garden that could print half of your salary each month without working for it, meaning you could spend not only your salary but half as much again, and retailers are service providers knew it – then spare money would be chasing goods and services which are of course limited.

Causing…. that’s right. I N F L A T I O N. Lots of money chasing few goods means the prices of those goods go up. Think van prices during lockdown, second hand car prices

Imagine that everyone had a similar machine. Do you think goods and services might start to increase in price?

Too much money chasing limited goods and services is a major cause of the inflation we see now. Money printing is one part of it, but it’s compounded by low productivity and as we see now by energy policy.

All of these things can be managed by Government, that is their job.

Inflation is by design. On this occasion it is helping to reduce the effect of UK Government debt – inflation erodes the value of money. Making debt less. In the last few years the Bank of England has introduced.

I have just realised how distrustful all of that sounds. But, like you, I wish it wasn’t true.

Banking Crises.

There are plenty of concerns about the banks at the moment.

These fall into several areas.

- Banks may make too many risky loans. When banks make loans to borrowers who are unlikely to be able to repay them, they are taking on too much risk. This can lead to a loss of confidence in the banking system, as people worry that their savings may not be safe.

- Banks may not have enough money to meet their obligations. Banks are required to keep a certain amount of cash on hand to meet the needs of their customers. If they do not have enough cash, they may not be able to meet their obligations, which can lead to a crisis.

- Banks may be exposed to too much risk from other banks. Banks often lend money to each other. If one bank fails, it may cause problems for other banks that have lent money to it. This can lead to a crisis, as banks may be reluctant to lend money to each other, which can make it difficult for businesses to get the loans they need.

All of these things were supposed to be sorted during the last crisis, 2008. These were sorted because ‘banks were too big to fail’. My bet would be the same will happening this time I feel sure.

I guess, like me, you are wondering how this happens. So I’ll explain my view.

Banks want to be treated as independent organisations, freewheeling along, doing what they want to make money. Want regulation to leave them alone.

Until it goes wrong. Interest rates go against them, some companies fail and leave them indebted (sometimes to other banks as well) and then they ask for ‘bail ins’ from the taxpayer – due to the mess they will obviously leave behind on failure. For the second time in my thirty years it looks like they will get what they want.

My advice to the banks…

- Banks should be more careful about the loans they make. They should only make loans to borrowers who are likely to be able to repay them.

- Banks should keep more cash on hand. This will help them to meet their obligations, even if there is a crisis.

- Banks should be less exposed to risk from other banks. They should limit the amount of money they lend to other banks.

Not bloody complicated is it.

New regulation is needed.

Until that happens, be careful.

Book Recommendation

I never ever thought I’d be running a book club. But…

If you want an enthralling story about nature, and it’s impact on this world Then Entangled Life by Merlin Sheldrake is brilliant.

It’s about mushrooms and funghi. It’s brilliant. If only humans could be more like these. Or perhaps we are. Go read it, you’ll thank me.

Pension Scheme Liabilities

Successive Governments have been ignoring a collosal and overwhelming pension liability that seems no sign of slowing down.

There are very few employees that have access to ‘defined benefit’ pensions schemes. These are pensions that provide a guaranteed pension on retirement. It was Gordon Brown who put the final nail in the coffin for that last of the schemes.

But the public sector, Government employees still have them and the guarantee is underpinned by you the tax payer. I wrote about this some time ago and tried to convince a select commitee that change was needed. Part of this is on the FT

In this I cover some of the issues. Both for our State Pension, normal pension schemes and of course the issues with unfunded pension schemes which make up the schemes for all public employees and poorly designed for our modern world.

For most of us who are 55 plus will not be affected by this, but those below us will end up with a shock as the costs of many schemes will overwhelm the system if left unchecked. There will simply not be enough tax collected in order to support the benfits that are due to be paid.

How Big Is The Problem?

The UK government’s pension scheme liabilities are the amount of money that the government owes to its employees and retirees. These liabilities are made up of the following:

- Defined benefit pensions: These are pensions that are based on a worker’s salary and years of service. The government promises to pay a certain amount of money each month to retirees, regardless of how much money they have saved.

- Other pension liabilities: These include things like survivor benefits and lump-sum payments.

The UK government’s pension scheme liabilities are a significant financial obligation. In 2020, the government’s pension scheme liabilities were £6.4 trillion. This is equivalent to about 224% of the UK’s entire an annual GDP (Source Google Finance +).

The government’s pension scheme liabilities are a growing problem. The population is aging, and more people are retiring. This means that the government will have to pay out more money in pensions. At the same time, the government is facing a number of financial challenge. These challenges will make it difficult for the government to meet its pension obligations.

The government is taking steps to address its pension liabilities. For example, the government has raised the retirement age and introduced a new pension scheme for public sector workers. However, these measures will not be enough to solve the problem. The government may need to take further steps, such as cutting spending or raising taxes.

Question is, we have record levels of taxation at the moment – how high can they go. Oh and the issue with inflation ‘inflating away liabilities’ doesn’t work for pension liaibilities because – they are full inflation linked under the scheme rules. This means the taxpayer is on the hook for the full amount, in real terms.

John Ralfe (according to Private Eye is the UK’s most eminent pension adviser, agree that all of this adds up to a massive problem. Part of his article on the subject is here.

None of this is easy to solve. Pensions are part of terms and conditions of employment, the problem is this is not the only issue we have to face as nation. Sure there is plenty to go around in the scheme of things. I just can’t help but think we need a new way, different thinking if we are to solve all of this.

Perhaps that’s just me. Let me know

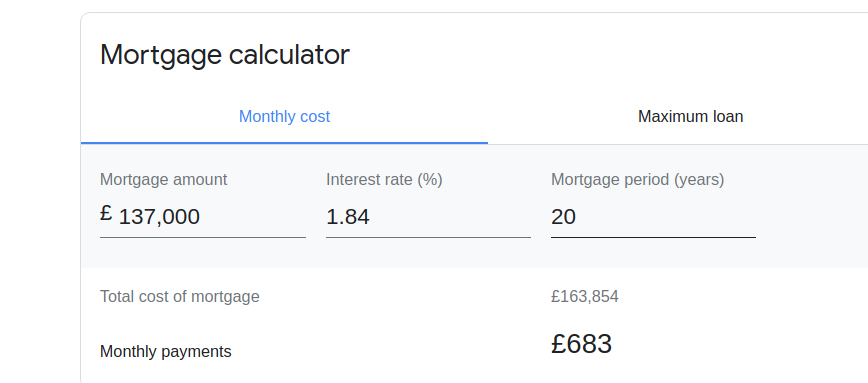

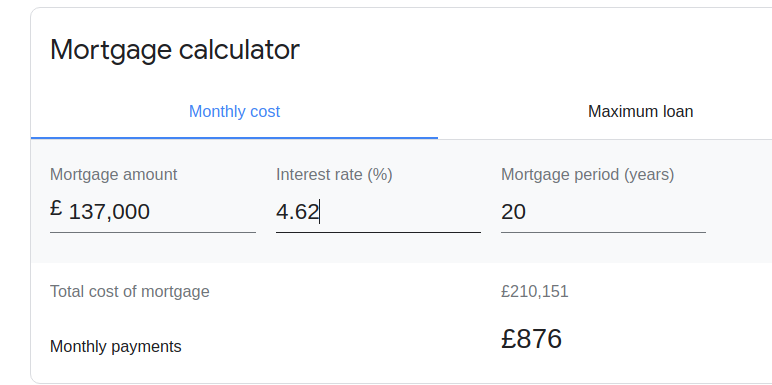

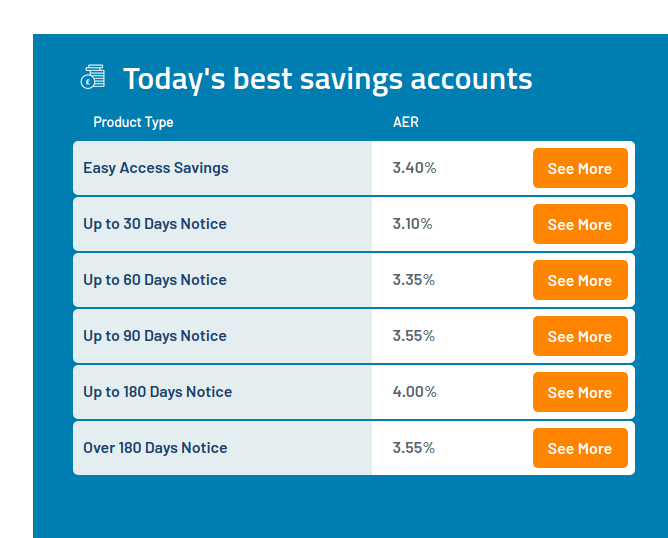

Mortgages and deposit rates.

Average mortgage costs some months back were …

Today

Based on a two year fix. And that’s before the latest interest rates start to impact.

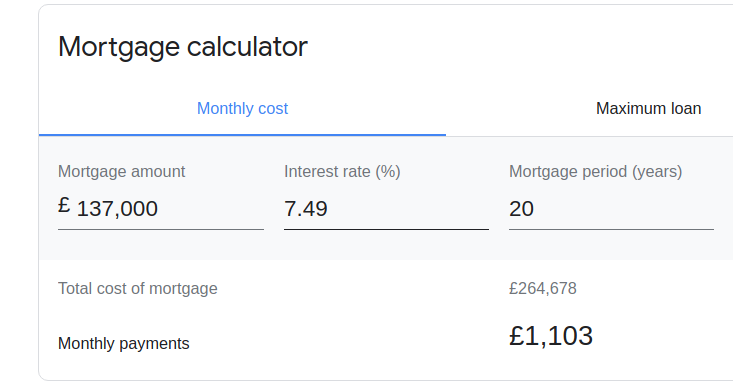

But, wait for it.

For borrowers on the SMR – Standard Mortgage Rate with the likes of Nationwide.

Ouch. Good news is, rates for savers have increased.

Source (New Website) https://moneyfactscompare.co.uk/savings-accounts/

That’s it from me.

Let me know if you are stuck with anything.

Richard