I think the whole Zahawi issue proves that were are in the middle of a massive decline – end of Rome style, politicians don’t care and do what they want. Where the shops and business are closing at record rates, the £ against the Euro is now 1.11 meaning imports like food from Spain will be increasing in cost quite dramatically and at the same time the FTSE 100 index hits record a record high.

Some of this was covered by Douglas Murray in his book the Slow Death of Europe from a few years back.

I didn’t think Douglas was right when I first read it, but it does seem to be right in many aspects. And we are in a lot of trouble of when it seems that the likes of Tommy Robinson and Katy Hopkins raise the alarm and seem to be right more often than wrong – interesting times ahead.

The read of the month is about a man who started Ballroom Dancing in his 80’s and has had run-ins with the neo-Darwinists since the 1960’s. I am not a religious man by any means, but I am thinking that the Darwin model doesn’t answer all of my questions.

Denis does have some alternative facts on the matter.

This is the link Denis Noble.

Good News For Savers.

On the 2nd of this month the Bank of England met to do something with interest rates and increased them to 4%, this it claims is to curb inflation that is primarily caused by…

I don’t know any more. It seems that nothing makes sense. But there is it. Good news for savers, bad news for those renting or buying homes.

Not so good news. As I suspected, we are seeing all the High Street lenders making sure their margins stay high.

Nationwide, as an example. Are charging 6.99% to borrowers on their standard rate and a whopping 5.5% for their other base lending rate. They call these Standard and Base Mortgage Rates and depending on when you started your mortgage with them and not on a fixed rate or tracker. You will be on one or other of these rates.

The Santander equivalent is 6.75%. (Ouch). Just not as ouch’ie as Nationwide.

It is likely they will both move to increase by at least .5% making them even more ouch’ie 7.4%. It’s all starting to feel like 1988 again.

I think it’s fair to compare the deposit rate of .75% with the standard variable rate of 6.99% which means Nationwide has a margin of 6.24% and Santander (deposit rate) .55% with a margin of 6.25%.

No wonder they always have polished uniforms and expensive CEO salaries. £6.4m for Santander’s boss and Nationwides’ Debbie Crosby a derisory £1.3m (with £3m odd with bonuses). How about that for fairness and equality.

It used to be the case that margins like this were for the lucky few organisations, not on the High Street. As organisations needed more money to lend they tightened margins (paid more to savers) it would seem that they have a plenty of money sloshing around or they would tighten their margins. I hope these narrow in the coming months that will be of benefit to all of us.

Importantly, if as expected the Bank of England increases rates again then the 8% mortgage could be back.

Links at the bottom.

I have more than a passing interest in financial inequality.

There is a growing wealth gap between those that have and those that do not. There is also a widening gap between the stupidly wealthy who seem to be able to manage their taxes and those that can’t.

I am not sure how this ends. Badly I think.

If you have more than an interest in economics in the world since 2008 then – Gary’s Economics will give you some interesting insights. He has recently been on Politics Daily (BBC) well worth a listen to some of his stuff.

This is what my Money Trainers project is all about – giving something back and educating as many as possible. As I explained it to my kids – if you remember the birds and bees conversation – then Money Trainers is the parent child conversation about money.

I think I had the idea before Gary, but we need as many of us a possible telling the truth about money.

On the subject of inequality. Last month I mentioned the use of Family Investment Companies and the planning options. These are one of the tools used by the very wealthy to swerve taxes not only in the UK but globally.

Interesting to see that the Inland Revenue is taking a keen interest in their use and of course combined with Family Trusts. It seems that Nadhim Zahawi has been playing the game with some of these planning options, as reported in the Sun newspaper. But reported in the Guardian as far back as 2017.

“A minister has insisted no evidence has emerged of “inappropriate behaviour” by former chancellor Nadhim Zahawi after he allegedly paid millions in tax to settle a dispute” As reported in the Wandsworth times. There is a fine line between avoidance and evasion.

It looks like a settlement has been made in order to avoid quite a lot of negative publicity.

I urge you to use them wisely and pay taxes in the correct way. Efficiently taxed investments doesn’t have to mean taxes avoided.

Interesting to note that his fine from the revenue was as high as 30%. Which kind of indicates some previous wrong doing, normally we can report missing income or gains up to six years without penalty for a first offence.

But now he’s gone – but still an MP. I wonder if there is an emoji for absolutely flabbergasted, if there was I would have inserted it here. Oh and that register of overseas interests. The list of beneficial owners of property, that should have been up to date by 31st January, isn’t. I know, that is something that surprises you!

Dying To Know

Over the last couple of months, I have working with the Indigo Umbrella group on a series of events called Dying to Know. These are group workshops where the whole end of life stuff is discussed.

Two things have come out of this.

Probate

Rehearsal

Firstly. Probate.

This little understood area of our lives is often just handed over to a local legal firm and the invoice paid, often taking months and at eye watering costs for an administration job. The DIY option is not complicated and is little more than a paper chase for many estates.

For sure, there are complex matters to be sorted with some. With the new online processing, it is a lot easier than it was even a few years ago. If you have ever submitted a paper application, then you’ll know how hard that was – online will be a ‘walk in the park’ for you.

If you feel confident in your ability to handle the probate process and have the time and resources to do so, you can apply to be the personal representative (also known as the executor) of the deceased person’s estate. This involves obtaining a grant of probate, which gives you the legal authority to deal with the deceased person’s assets.

There are several steps involved in dealing with probate following a death. Depending on the individual’s estate, the process can vary vastly.

The first steps are typically to obtain the death certificate, inform creditors of the individual’s passing, and then make an inventory of the estate’s assets.

Once all the missing paperwork and details have been obtained, an application must be completed and submitted to the probate court.

Remember, the only reason the Probate Office exists…

… to make sure the right amount of tax is paid. For those estates below the tax thresholds, the process is quite simple.

For those that don’t want the paper chase, I do offer a fixed price service (pay monthly) to deal with everything on behalf of the executor. No surprises, with cases turned around in about 8 weeks (Probate Office dependent).

Rehearsals for Death.

One of the exercises I got everyone to do at the Dying to Know event was a rehearsal for the days after death. Assuming one of them wasn’t there, they had died in the days before.

Working out, are Wills signed and witnessed, who has access to the online banking, where are the deeds to the house, pension and investment documents. An hour or so working out what is missing, what information is not known.

It might seem a bit morbid, but it makes practical sense. I did it with my other half, and we had a bit of fun rummaging through papers and talking about the good old days. If for no other reason, it forced me to clear some papers and post some old photographs and bits of history to people I hadn’t spoken to for a while.

Give it a go.

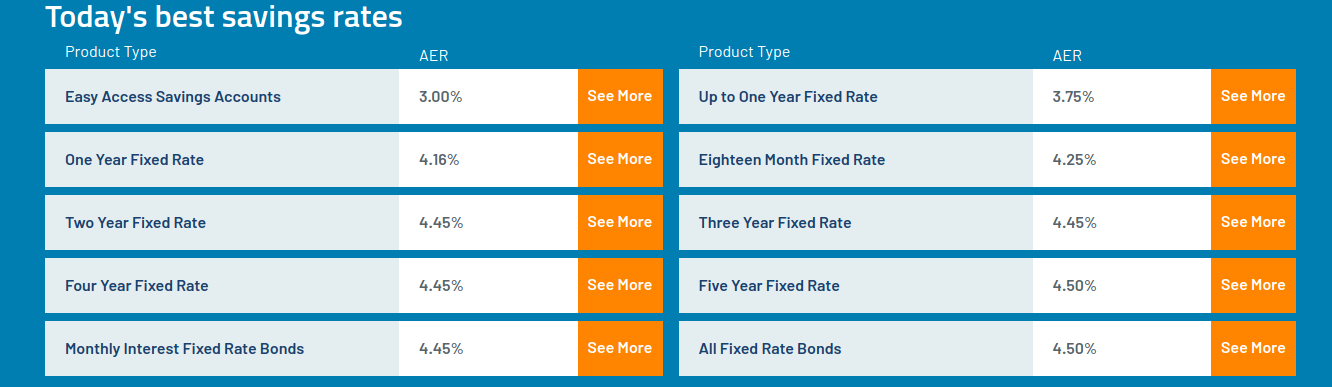

Current Best Buys from MoneyFacts.co.uk

Expect these to increase in the coming couple of days.

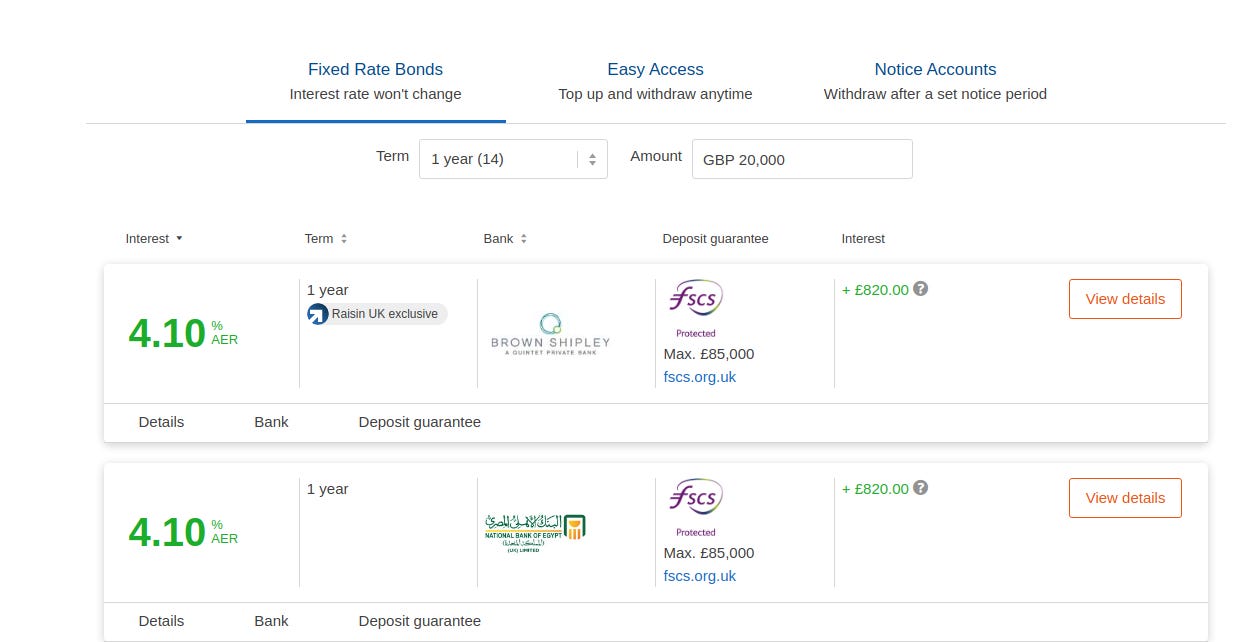

Hargreaves Lansdown have recently made changes to their ‘one place’ savings product. Basically means you can have one umbrella account with them and invest in range of accounts without the hassle of many online logins or administration hoops to jump through.

Not all of the deposit takers in the marketplace are on the system but the Compensation Scheme does apply, and I think this is the future for at least part of the ‘where do I put my money’ conundrum. Especially as the world we live in is more complicated than ever.

There is also Raisin – this has been around for a while. Basically a group of European banks on the platform that works in a similar way to the Hargreaves product, but with 3.5% available on short term deposit (6 months).

Again, these look likely to increase in the coming days.

Until next month.

Richard

PS As always, please get in touch if you have any queries.

Links